COLDWELL BANKER®

Buying a home is one of life's biggest investments and most exciting adventures. With my trusted network of affiliates, I’ll be your dedicated partner, guiding you through every step to ensure a smooth and successful experience.

This Home Buyer Guide includes helpful information to get you started:

When you choose me to represent you, I'll be by your side every step of the way, giving you the insights and information you need to feel confident in your decision. I will:

The first step in any home search is finding out exactly how much home you can afford and securing the financing to make the purchase. While you can get a rough estimate through prequalification, taking the extra step to obtain pre-approval will give you some added advantages.

Pre-approval helps you:

When you find a home you love and are ready to make an offer, your mortgage pre-approval lets the seller know that you're serious and fully prepared to buy their home, putting you in a stronger position than other potential buyers.

Here are some of the documents that you will need to provide your lender to get the pre-approval process started:

The first stop on your home search? My website. Not only is it an easy way to check out all the available properties in your preferred area, but it's also a great way for me to get to know the types of properties you like. Simply register on the site, and I'll receive updates about your activity. Plus, you can save your search for future access, save and share homes you like, and sign up to receive email alerts when new homes that match your criteria come on the market.

And thanks to its responsive design, you can do it all from your mobile device, tablet or desktop!

Make your online home search easy with one website that gives you access to everything home buyers need.

With my website, you can:

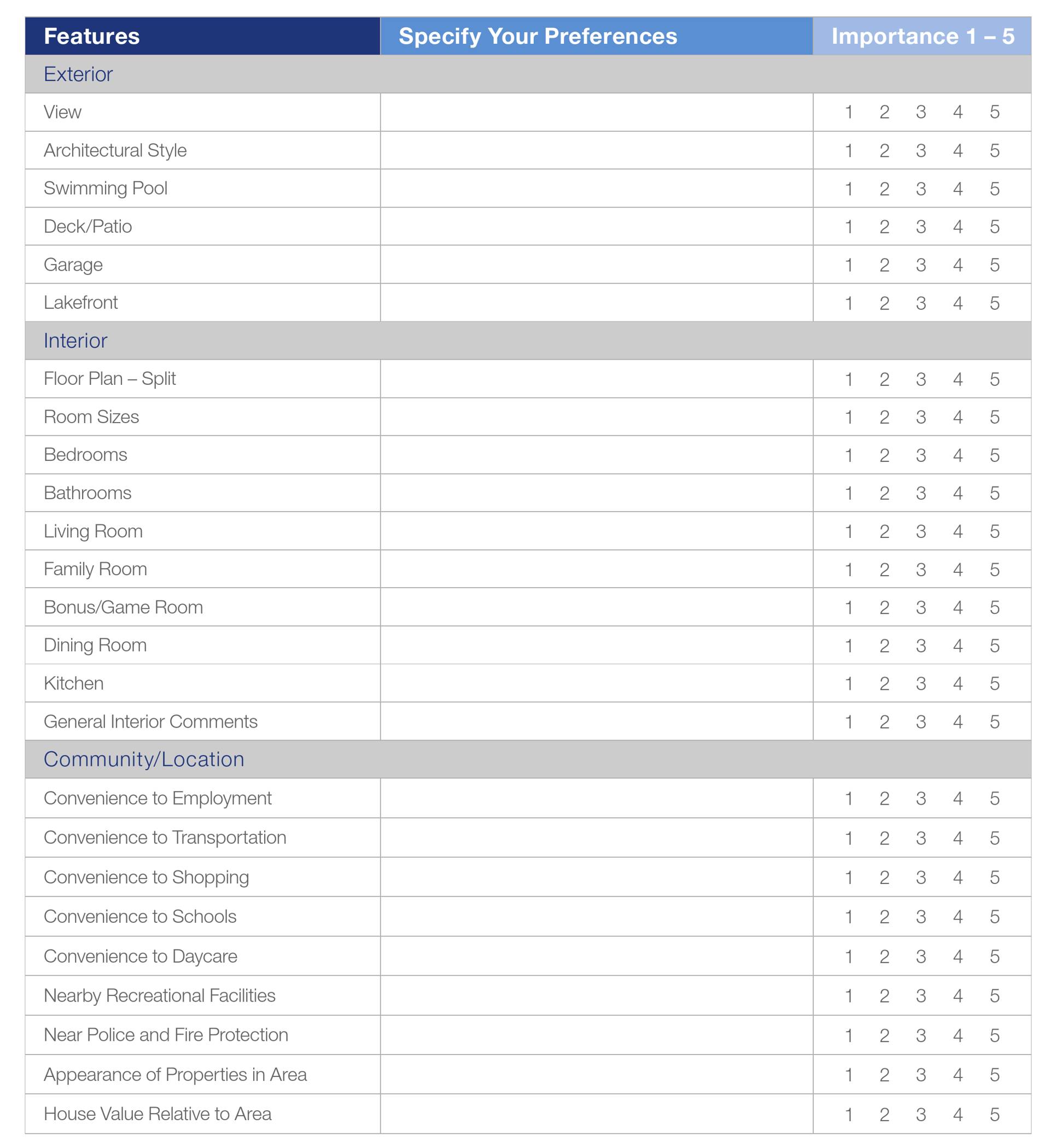

The more I know about the type of home you want, the better. Take a minute to think about the features your new home must have, as well as what you'd ideally like it to have, and let’s talk it over.

There are many factors that influence the market value of a home. I'll provide you with the insights and information you need to make an offer you're comfortable with. Some of the factors to consider include:

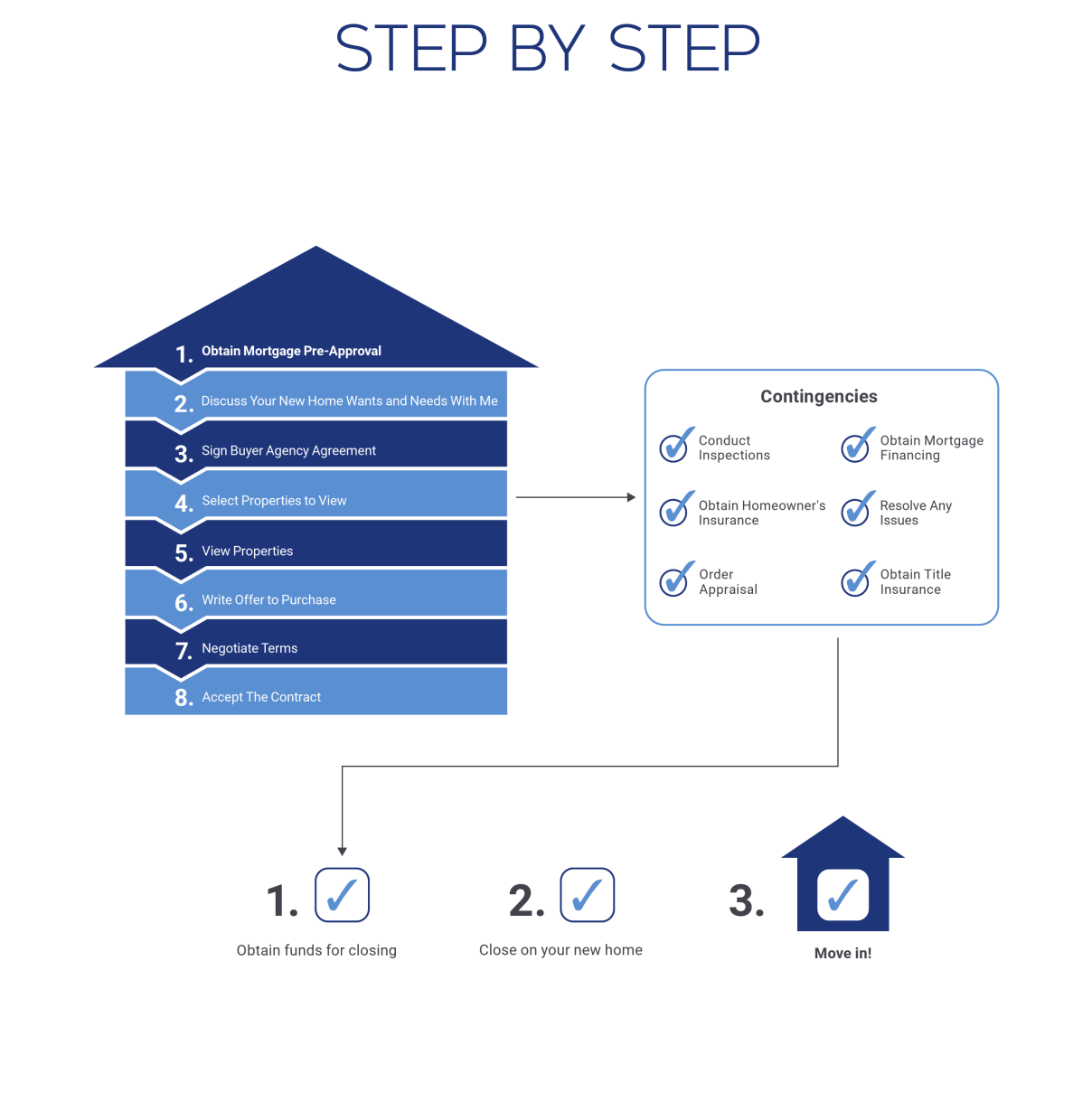

Once the offer is written, I will present it to the seller's agent. At that point, the seller can accept your offer, reject it, or counter it to start the negotiation process. I'll work with you to plan a strategy to ensure the most advantageous terms and pricing that fit your budget.

Once your offer has been accepted, the closing process begins. Here are some of the typical steps involved.

Home inspection - Most property sales are contingent on the results of a home inspection, which is paid for by the buyer. The inspection typically occurs within 10 days of offer acceptance, and includes a review of the home's exterior elements like the roof, siding, trim and windows, as well as kitchen and bathroom fixtures and appliances and major systems like heating and cooling, plumbing and electrical.

If defects are discovered during the inspection, you may exercise the remedy described in your offer or negotiate with the seller to determine what repairs will be made.

Title search – This is a historical review of all legal documents relating to ownership of the property to ensure that there are no claims against the title of the property. It is also recommended that you purchase title insurance in case the records contain errors or there are mistakes in the review process.

Appraisal - As a standard part of the

mortgage process, your lender will order an appraisal report to ensure that the loan will be guaranteed by the home's value.

Final walk-through - If it's requested in the contract, you'll be given the chance to look at the home to make sure it's in the same condition as when you signed the sales agreement.

Closing costs - In addition to your deposit and down payment, there are a variety of other costs involved in closing including:

Your transaction forms for the purchase of your new home will be entered into HomeBase®, a convenient, secure website where you can track the progress of your sale and access your documents throughout the process, and long after the closing.

Homebuyer's Glossary